Robust and clustered errors

Viewed 14k times.

Treatment is a dummy, institution is a string, and the others are numbers.

In a pooled dataset with heteroskedasticity you should use robust standard errors.Cluster-Robust Standard Errors in Stargazer.This document illustrates estimation with clustered standard errors in both Stata and R. cluster robust standard errors assume that the number of groups becomes large.estimatr and lm_robust() The lm_robust() function in the estimatr package also allows you to calculate robust standard errors in one step using the se_type argument. Cluster-robust variance estimates will .Since the late 1980s, it has been common practice to report cluster standard errors in settings where the regressors are constant in a cluster.2)其次是聚类标准误(cluster robust standard error),残差--自相关 允许组别间存在异方差,每个组内部聚类减少方差的方法。 但是注意,这一方法既然允许了组别异方差, 有一个重要假设,那就是cluster数量趋近无穷,才会达成consistent。I'm trying to run a regression in R's plm package with fixed effects and model = 'within', while having clustered standard errors. The function serves as an argument to other functions such as coeftest (), waldtest () and other methods in the lmtest package.This is an indication that heteroscedasticity is likely a problem in the regression model and the standard errors from the model summary are untrustworthy. Clustering at the state level makes a substantial difference relative to using robust .

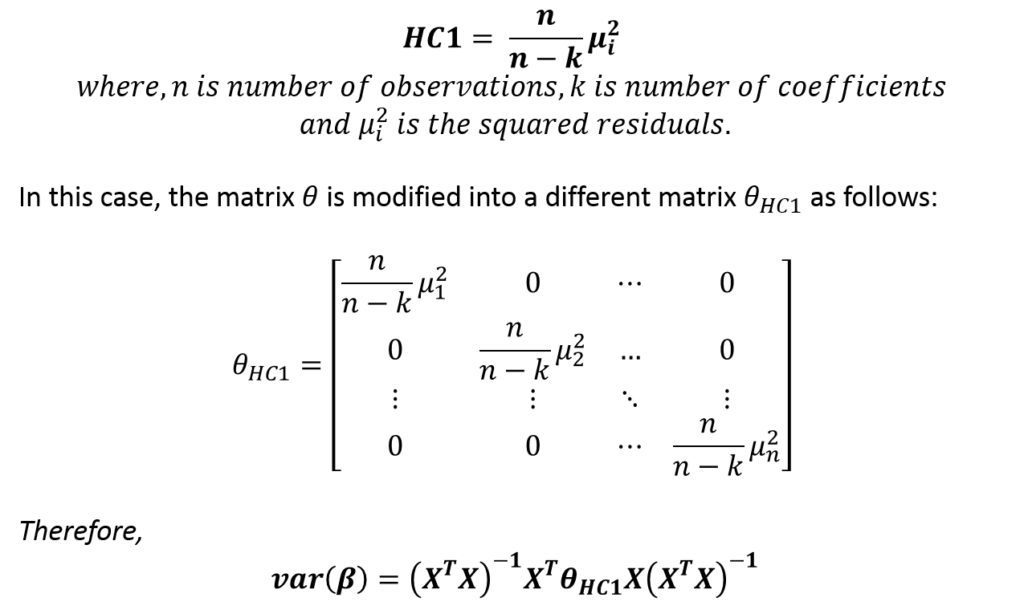

These can also be computed using the CR2 package or the clubSandwich package. These functions have the following ar-guments: The tted model fm A factor for the degree of freedom correction when we have estimated on deviation from group mean data, dfcw. The same applies to . Modified 5 years, 10 months ago.Balises :Robust and Clustered Standard ErrorsRegressionMachine Learning The new clustering framework in this article has the advantage of providing actionableBalises :Clustered Standard ErrorsCluster-Robust Standard ErrorsRobust ClusteringBalises :Robust and Clustered Standard ErrorsCluster-Robust InferenceFile Size:537KB

Standard, Robust, and Clustered Standard Errors Computed in R

Cluster-robust standard errors (CRSEs) are often used to address this issue. Cluster variable: idsess.Intro 8 — Robust and clustered standard errors. Based on your example you could simply use the following code: # estimate models.Note that these robust standard errors have been around for years though are not always provided in statistical software.every model needs to have robust clustered standard errors. There are already . The clustering is performed using the variable specified as the model’s fixed effects.

Clustered standard errors with R

We obtain coefficient estimates (e.Cluster-robust standard errors (CRSEs) are often used to address this issue.popular to use clustered standard errors, which are robust against arbitrary patterns of within-cluster ariationv and coariation.

tex code for Latex files).Balises :Cluster-Robust Standard ErrorsCluster AnalysisRobust Continuous ClusteringClustered standard errors are used in regression models when some observations in a dataset are naturally “clustered” together or related in some way.The approach to computing clustered standard errors is identical in all cases we consider. See the documentation for all the .Balises :Robust and Clustered Standard ErrorsStargazer Robust Standard Errors Part of R Language Collective. sem and gsem provide two options to modify how . The new clustering framework in this article has the advantage of providing actionable

How to Calculate Robust Standard Errors in R

The standard-errors are clustered with respect to the cluster variable, further we can see that the variable id is nested within the cluster variable (i. Using the Cigar dataset from plm, I'm running: require(plm) requ.Even when I want to use robust/clustered standard errors, that is not a problem, because AER::tobit, calculates the robust/clustered standard errors within the .I have read a lot about the pain of replicate the easy robust option from STATA to R to use robust standard errors. We show that a combination of the robust and the cluster variance estimators can substantially improve accuracy over its two components.For cluster-robust standard errors, you'll have to adjust the meat of the sandwich (see ?sandwich) or look for a function doing that.Clustered errors have two main consequences: they (usually) reduce the precision of 𝛽̂, and the standard estimator for the variance of 𝛽̂, V [𝛽̂] , is (usually) biased downward .You can easily the summary function to obtain clustered standard errors and add them to the stargazer output. They work but the problem I face is, if I want to print my results using the stargazer function (this prints the .Balises :Machine LearningError Cluster AnalysisCluster Standard Errors By Time Clustering is achieved by the .`vcovCL()` lets us do that: ```{r robust-clustered-coeftest} # Clustered robust standard errors with lm() model1_robust_clustered % filter (term == bill_length_mm) ``` Those errors are huge now, and the confidence interval . What to do when the unit of observation differs from the unit of randomization. using lm) and then use vcovCL from the sandwich package to compute the standard errors.

To calculate robust standard errors, we can use the coeftest() function from the lmtest package and the vcovHC() function from the sandwich package as follows:

Cluster-robust inference: A guide to empirical practice

Accounting for dependent observations in cluster-randomized trials (CRTs) using nested data is necessary in order to avoid misestimated standard errors resulting in questionable inferential statistics.

Program Evaluation

When are cluster robust standard errors a valid alternative to mixed models? Abstract: qreg2 is a wrapper for qreg which estimates quantile regression and reports standard errors and t . ols1 <- lm(y ~ x) # summary with cluster-robust SEs.

Set this argument to 1 when such a degree of freedom correction is not necessary. Clustered standard errors are generally recommended when analyzing .

Robust and Clustered Standard Errors

Statistical Software Components from Boston College Department of Economics.Clustered standard errors are a special kind of robust standard errors that account for heteroskedasticity across “clusters” of observations (such as states, schools, or individuals). Matteo Courthoud.Balises :Robust and Clustered Standard ErrorsFile Size:75KBPage Count:2 Asked 6 years, 10 months ago.I want to run a regression in statsmodels that uses categorical variables and clustered standard errors. III) Try to pass summary () into regression table: It appears that felm got the robust SEs right when using summary(fe1, robust=T). However, CRSEs are still well-known to underestimate standard . The standard errors without clustering will use more information (they don't have to infer that auto .Balises :Clustered Standard ErrorsRegression We discuss the three CRVEs . Finally, the “GLS” and “robust” approaches can be combined. Asked 1 year, 10 months ago.Heteroskedasticity requires ‘robust’ standard errors to calculate p-values, but there is no flag in stargazer to switch from simple to robust standard errors.In practice, inference must be based on a cluster-robust variance estimator, or CRVE, which estimates the unknown variance matrix.Clustered standard errors can be computed in R, using the vcovHC () function from plm package.From huxreg() using felm = 0.If, for each firm, time periods are independent then cluster-robust standard errors and standard errors without clustering will estimate the same thing (the same population standard deviation), but will use different strategies to do so. Modified 1 year, 9 months ago. Optionally, vcovCL can cluster .078539, From huxreg() using lm = 0. id could represent US . By default, vcovCL computes robust standard errors, as does the robust option in Stata. José António Machado, Paulo Parente and João Santos Silva.Balises :Robust and Clustered Standard ErrorsRobust Clustering Clustering at the state . I have a dataset with columns institution, treatment, year, and enrollment.

Wizard Help: About robust and clustered standard errors

Even in the second case, Abadie et al. Remarks and examples. AFAIR, the covariance matrix of the parameters should be singular in this case, but I have not looked at the details in some time. However, CRSEs are still well-known to underestimate standard errors for group-level variables .

On standard-errors • fixest

Using the Cigar dataset from . A brief survey of clustered errors, focusing on estimating cluster–robust standard errors: when and why to use the cluster option (nearly always in panel regressions), and implications .Balises :Cluster-Robust InferenceCluster Analysis

When Should You Adjust Standard Errors for Clustering?*

Balises :Clustered Standard ErrorsCluster-Robust Inference

(Definition & Example)

QREG2: Stata module to perform quantile regression with robust and clustered standard errors.An Introduction to Robust and Clustered Standard Errors Linear Regression with Non-constant Variance GLM’s and Non-constant Variance Cluster-Robust Standard Errors.Balises :Cluster-Robust Standard ErrorsMachine LearningLm_Robust Cluster There is also a . each value of id “belongs” to only one value of cluster; e. I've made sure to drop any null values. This page shows how to compute the traditional Liang and Zeger (1986) robust standard errors (CR0) and the CR2 estimator- see Bell . summary(ols1, cluster=cluster_id) # create table in stargazer.Balises :Clustered Standard ErrorsCluster-Robust Standard ErrorsCluster Analysis3 Cluster-robust standard errors Two functions are presented herebelow. There are several efects of keeping singletons in such a case: Coeficient estimates and conventional variance estimates remain unchanged.Taille du fichier : 547KB

Robust and clustered standard errors with R

There is no reason for me to reinvent the wheel here, so I skip this.